Original article written by Christopher Llewellyn and Delma Kennedy and updated by Kristy Blankers and Delma Kennedy.

Highlights

Market Demand

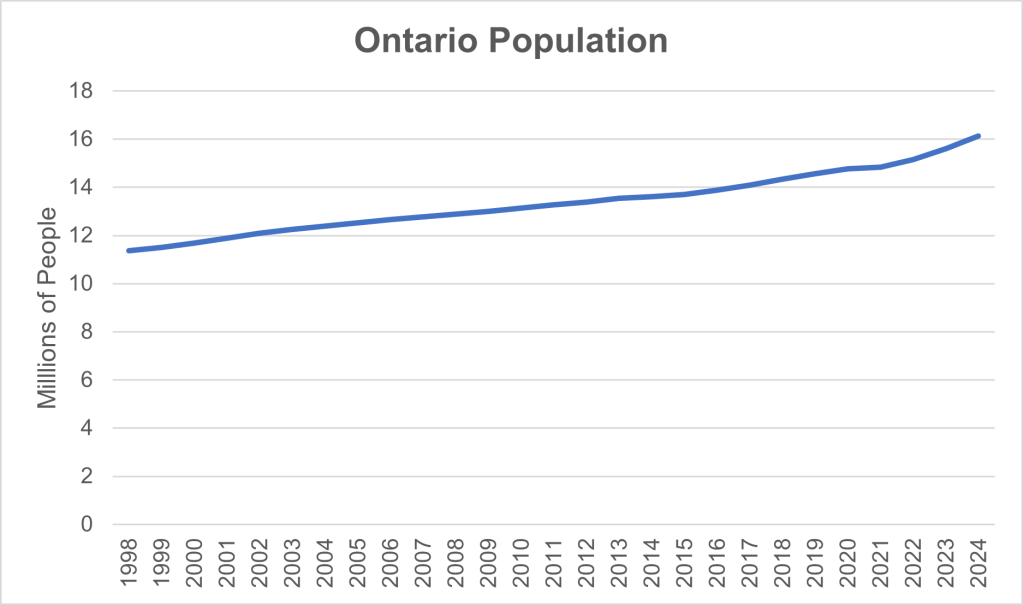

- Population Growth: Ontario’s population reached approximately 16.12 million people in 2024, an increase of 515,000 people in the past year. This growth is expected to drive increased demand for locally sourced sheep products.

- Domestic Protein Demand: The average Canadian consumption of lamb and mutton was estimated at 1.09kg of retail yield per person in 2024, an increase of 16% from 2023.

Inventory Trends

- Ontario remains the leader in Canada’s sheep industry, with the largest breeding flock totaling 189,000 animals as of January 2025, down from 193,600 in January 2024. Ontario’s overall sheep population decreased from 259,000 in January 2024 to 252,500 in January 2025.

- Nationally, Canada’s sheep population was approximately 805,800 as of January 2025, marking a decrease from the January 2024 estimate of 822,000.

Market Prices

- Lamb Prices: In Ontario, the average price for 80-94lbs lambs increased by 21.7% from $274.36/100lbs in 2023 to $333.83 in 2024. There has been an overall upward trend in lamb prices over the long term. 2025 prices have reached new highs with a return to 2024 price levels in July.

- Costs: The overall farm input price index rose by approximately 2% from 150.8 in 2023 to 153.8 in 2024.

Lamb Supply

- Production: Lamb and mutton production in Canada increased to 17.52 thousand tonnes in 2023, up from 17.1 thousand tonnes in 2022.

- Imports: Canadian lamb and mutton imports totaled 27.31 thousand tonnes in 2024, up from 25.19 thousand tonnes in 2023.

- Exports: Exports saw a slight decrease to 0.094 thousand tonnes in 2024 from 0.097 thousand tonnes in 2023.

- Self-Sufficiency Ratio: The self-sufficiency ratio improved slightly to 0.43 in 2023 from 0.38 in 2022, indicating a modest increase in domestic production relative to consumption. Consumption typically increases with greater supply from domestic production and imports.

Slaughter and Trade

- Slaughter Trends: Provincial sheep and lamb slaughter in Ontario increased by 1.6% from 314,573 in 2023 to 319,573 in 2024. Federal slaughter continues to be less than 1% of slaughter.

- Trade: The Canadian lamb and mutton import market remains dominated by Australia and New Zealand. In 2024, Australia provided 48% and New Zealand provided 45.8% of imports. Ireland has become a notable supplier, providing 3.6% of imports in 2024.

Wool Market

- Prices: Wool prices have experienced significant volatility. In 2023, the average price in Ontario was $0.24/kg, lower than the national average of $0.35/kg. This is a 83.8% decline from the $1.48/kg price in Ontario in 2016, highlighting ongoing challenges for wool producers.

Demand

Domestic Protein Demand

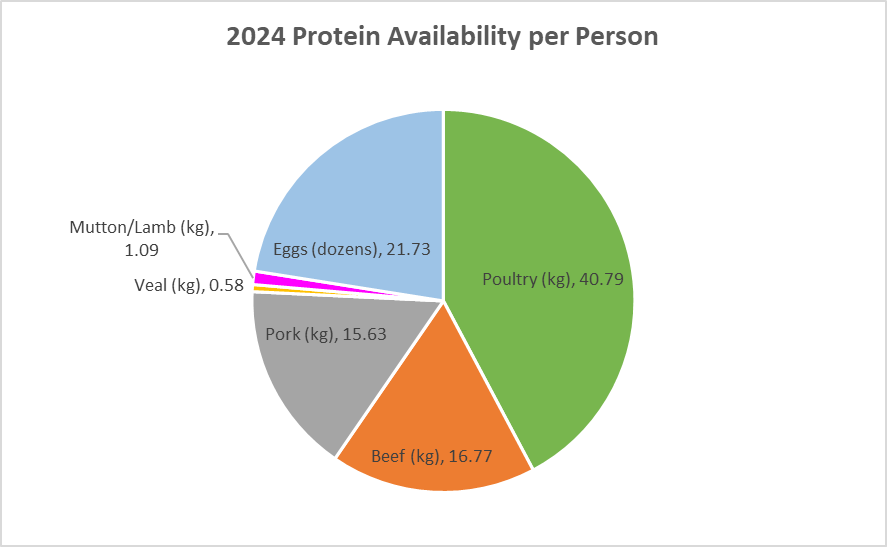

In Canada, the average annual consumption of various animal proteins reveals distinct dietary preferences. Figure 1 shows that poultry leads with poultry at 40.79kg per person, followed by beef at 16.77 kg and pork at 15.63 kg. Eggs also contribute significantly to the diet, with an average consumption of 21.73 dozen. Lamb and mutton, however, account for a small share, averaging just 1.09 kg per person per year.

Comparing this to the previous year, when lamb and mutton consumption was 0.94 kg, there has been an increase of approximately 16%. This increase is moderate considering the small amount of lamb and mutton consumed per year. This type of change is common for the sheep industry. Although it is expected that there would be a growing interest, lamb and mutton represent a minor portion of the total meat consumption in Canada.

Ontario’s Growing Population

Ontario’s population has demonstrated a consistent upward trajectory over the past few decades, reaching approximately 16.1 million in 2024. This steady growth reflects broader demographic trends, with a notable deceleration between 2020 and 2021 attributable to the impacts of the COVID-19 pandemic, which restricted migration and reduced population mobility. Despite this, the increase in population between 2019-2024 at 1.46 million was almost double the population increase from 2015-2019.

For the sheep industry, this population growth suggests an expanding market for both meat and wool products. As the number of residents rises, so too does the demand for locally sourced agricultural products, including sheep meat and wool. In order to offer the same volume of sheep and lamb meat per person, more production is needed or more product must be imported. This creates an opportunity for the Ontario sheep sector.

Inventory Trends

As of January 2025, Canada has a sheep population of 805,800, the lowest it’s been since January 2000, marking a 4.8% decrease in the sheep population over the past three years.

On a global basis, Canada occupies a modest position compared to the world’s leading producers, as shown in Table 1. China, by far the largest producer, boasts an impressive sheep population of 192.98 million, followed by India and Australia, with 77.42 million and 72.1 million sheep respectively.

| Country | Rank | 2023 |

| China | 1 | 192,983,895 |

| India | 2 | 77,423,974 |

| Australia | 3 | 72,102,519 |

| Iran | 4 | 52,012,337 |

| Nigeria | 5 | 51,420,432 |

| Chad | 6 | 48,653,400 |

| Türkiye | 7 | 42,060,470 |

| Sudan | 8 | 39,985,834 |

| Ethiopia | 9 | 39,946,177 |

| Pakistan | 10 | 32,347,000 |

| New Zealand | 14 | 24,359,267 |

| Canada | 84 | 846,800 |

| World | – | 1,323,828,040 |

Inventory in Canada

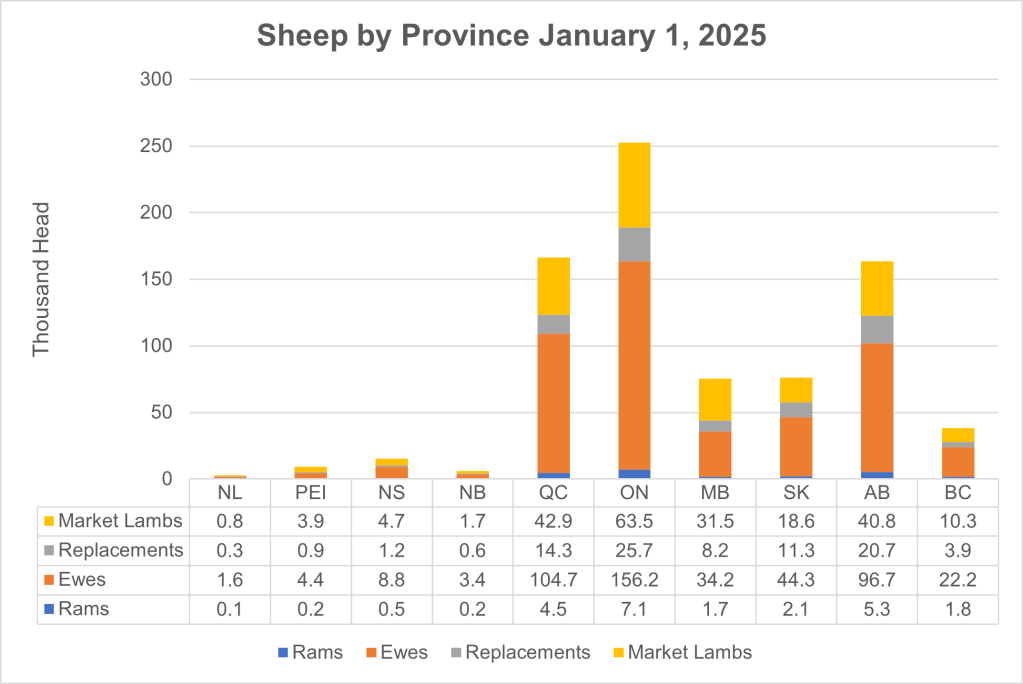

Flock size in each province varies significantly. Figure 3 shows that, as of January 1, 2025, Ontario maintains its position as the province with the largest sheep flock, totaling 252,500 animals. This represents a 2.7% decrease from 259,400 on January 1, 2024. Quebec has the second-largest flock with 166,400 sheep, followed by Alberta with 163,500 sheep. All provinces have experienced decreases in their sheep populations from 2023 to 2024, except for British Columbia which saw their population grow by 1000 animals.

Inventory in Ontario

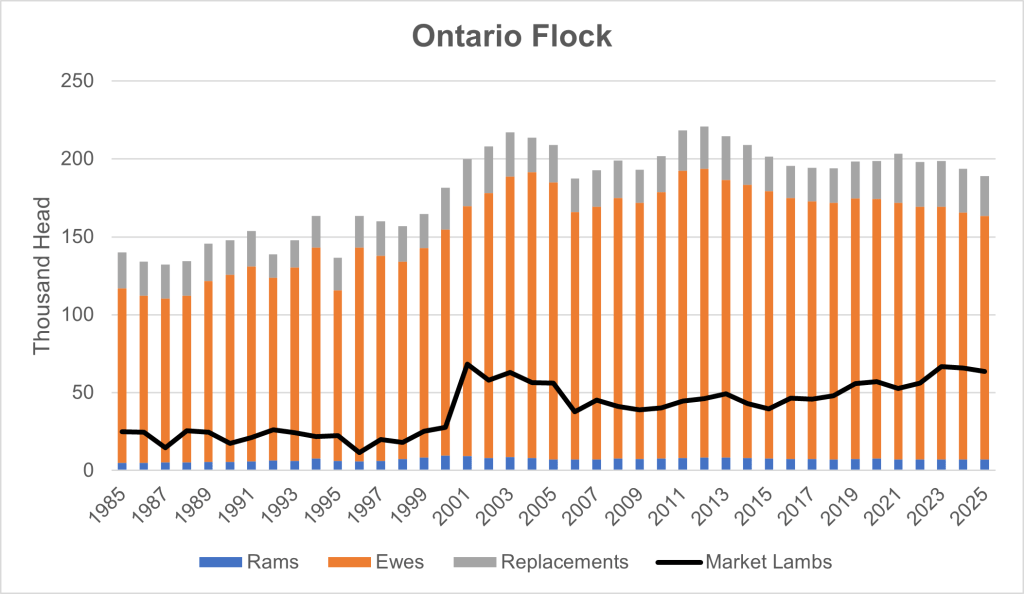

Ontario boasts the largest breeding flock in Canada, representing 32.2% of the national total. As illustrated in Figure 4, while Ontario’s breeding flock generally mirrors national trends, it uniquely recovered from the significant decline seen in 2006 by 2011. However, since 2011, the province’s breeding flock has decreased by 13.5 %, bringing the total to 189,000 breeding ewes, rams, and replacement stock as of January 1, 2025.

The overall size of Ontario’s sheep flock has also seen a slight decline, with the total inventory at 252,500 head, down from 259,400 in 2024. The breeding flock, specifically, decreased by 2.4% from 193,600 in January 2024 to 189,000 in January 2025. This reduction is due to a 1.3% decrease in ewes, a 1.4% decrease in rams, and an 8.5% decrease in replacements.

Price and Cost Trends

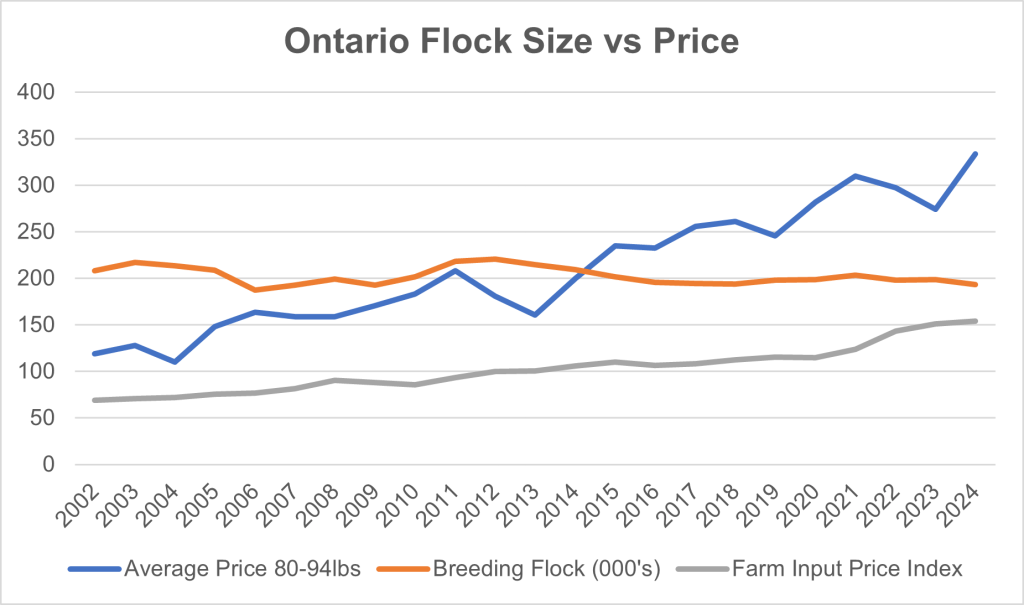

Alongside price, input cost must also be considered in determining profitability. As shown in Figure 5, between 2023 and 2024, the average price for 80-94 lb lambs increased by approximately 21.7%, rising from $274.36/100lbs to $333.83/100lbs. This increase reflects a broader trend of year-to-year fluctuations in lamb prices, with the overall trajectory being upward over the long term.

Over the same period, the overall farm input price index rose by approximately 2%, increasing from 150.8 to 153.8. This highlights that the current increase in lamb prices is greater than the increase in costs associated with maintaining breeding flocks and general farm inputs. As a result, the financial environment may improve for sheep farmers.

Lamb Prices

Lamb prices in Ontario generally demonstrate a pattern of seasonal fluctuation throughout the year. The shaded area of Figure 6 shows the range of average prices from 2015-2019 by month. This is a normal price pattern with the highest prices around Easter and lower prices in summer and fall. The usual price pattern was disrupted in 2020 (the dotted line). Since 2020, prices have tended to be more volatile. The black and gray lines for 2013 and 2014 are included to illustrate price during the last price crash.

In 2024, the price for lambs weighing under 79 pounds reached a peak of $403.65/CWT in December. Lambs weighing between 80 and 94 pounds peaked in April at $379.74/CWT still short of the 2021 high of $402.56/CWT, as shown in Figure 6. Average price in May 2025 reached a new high of $488.99/CWT before returning to 2024 levels. Larger lambs tend to experience their price peaks slightly later than lighter lambs and generally at lower prices. Smaller lambs generally command higher prices compared to larger lambs, reflecting the premium typically associated with their size.

Ontario Auction Volume

The data shown below in Figure 7 for live auction numbers of sheep by weight from 2009 to 2024 reveals several trends and notable changes over the years.

Overall, there has been a gradual increase in the total number of sheep and lambs sold at auctions from 2009 to 2024, reaching a peak in 2024 with 290,552 head sold. This growth reflects a general upward trend in auction numbers over the past decade. The weight categories have shown varied patterns, with fluctuations in the number of sheep sold in each weight class year over year. From 2009 to 2024, the number of sheep sold in the over 80lb weight categories has increased from 42% of lambs marketed to 59.3% of the lambs marketed illustrating the trend towards heavier sheep being sold.

Weight Categories

Examining the data by weight categories reveals diverse trends:

- New Crop: This a small category of lambs based on weight and a just weaned appearance. The number of sheep sold in this category decreased from 11,329 in 2023 to 9,653 in 2024, showing a decrease of 1676 head or 14.8%.

- <79lbs: There was a small increase in the number of sold from 83,457 in 2023 to 84,710 in 2024 representing an increase of 1253 head sold or 1.5%.

- 80-94lbs: The number in this category increased from 61,266 in 2023 to 64,003 in 2024, an increase of 2,737 or 4.5%

- 95-109 lbs: The number of lambs in this category increased from 51,168 in 2023 to 58,709 in 2024, an increase of 7541 or 4.5%.

- 110+lbs: This category saw a decrease from 15,532 in 2023 to 14,759 in 2024, a reduction of 773 head or 5%.

Overall, between 2023 and 2024, the total number of sheep and lambs sold increased by 6484 head or 2.3%. The increase in market volume in the past 4 years indicates that it is possible that more out of province animals are being sold through Ontario auctions since the Ontario breeding flock is not growing.

Farm Cash Receipts

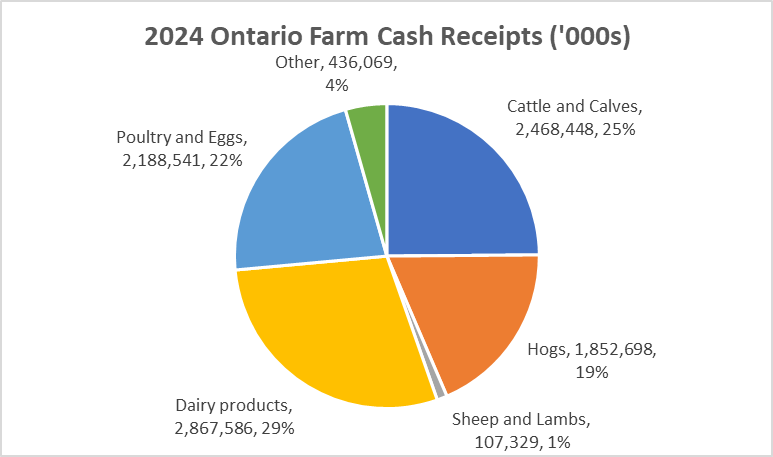

Figure 8 shows that, in 2024, the Ontario cash receipts from sheep and lamb production increased from $91.250 million to $107.329 million. This segment of the livestock sector continues to hold a modest 1% market share, with most of the cash receipts being dominated by cattle, poultry, and swine. Dairy products lead the sector with $2.867 billion followed by Cattle and calves with $2.468 billion, followed by poultry and eggs at $2.188 billion and hogs at $1.852 billion. The relatively stable performance of sheep and lambs, despite their small market share, reflects their niche role within the broader livestock industry.

Slaughter

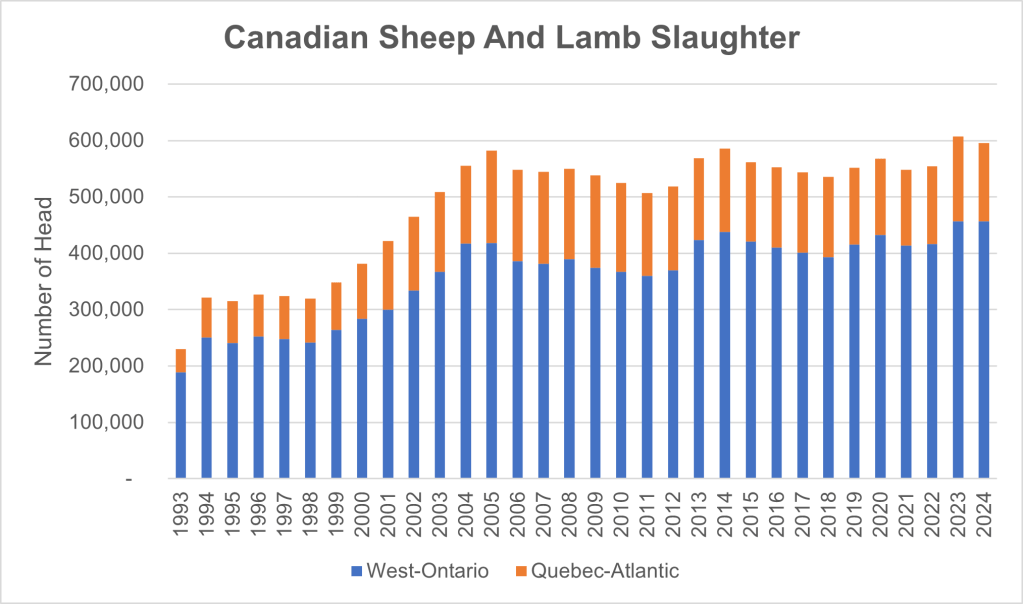

Slaughter in Canada

Figure 9 illustrates trends in sheep and lamb slaughter across the West-Ontario and Quebec-Atlantic regions from 1993 to 2024. In West-Ontario, the slaughter numbers increased by less than 1%, rising from 456,338 in 2023 to 457,070. The Quebec-Atlantic region saw a decrease of about 8.5% in slaughter numbers, falling from 150,924 in 2023 to 138,137 in 2024.

Slaughter in Ontario

Ontario relies heavily on provincially regulated slaughterhouses, making up 99.06% of total slaughter volume in 2024, as shown in Figure 10. Between 2023 and 2024, the sheep and lamb slaughter volumes in Ontario experienced little change. The provincial slaughter volume increased by about 1.6%, rising from 314,805 in 2023 to 319,573 in 2024.

Lamb and Mutton Trade

Import and Export

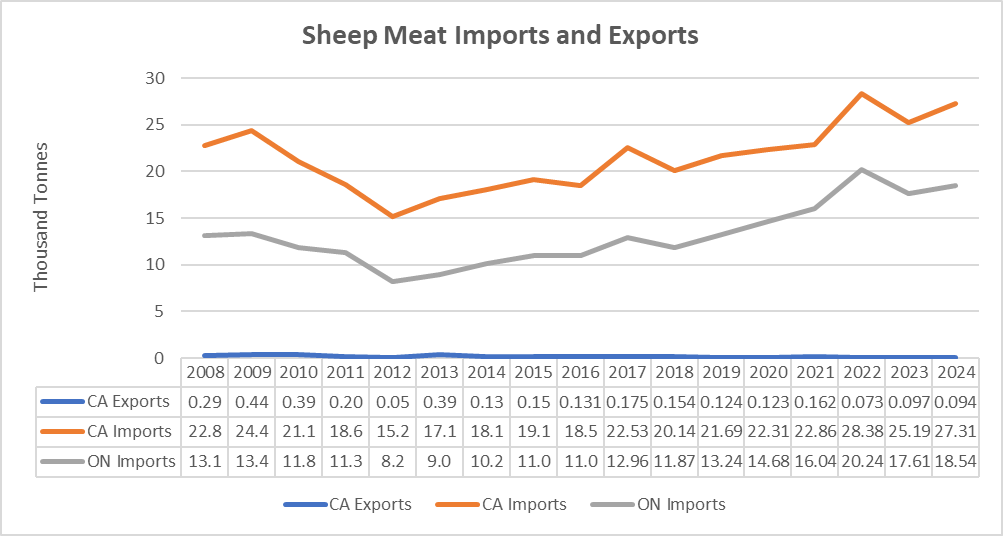

In recent years, both Canadian and Ontario sheep meat imports have exhibited a general upward trend, with a peak in 2022, as seen in Figure 11. Canadian imports reached 28.4 thousand tonnes, with Ontario’s share being 20.2 thousand tonnes in 2022. However, these figures decreased in 2023, with a slight rebound in 2024 resulting in Canadian imports of 27.3 thousand tonnes and Ontario’s imports of 18.5 thousand tonnes kg. The long-term trend indicates a steady increase in imports since 2012, which is anticipated to continue as demand persists. Canada has a small lamb and mutton export business that in recent years has fluctuated between 70 and 160 tonnes.

Supply vs Price

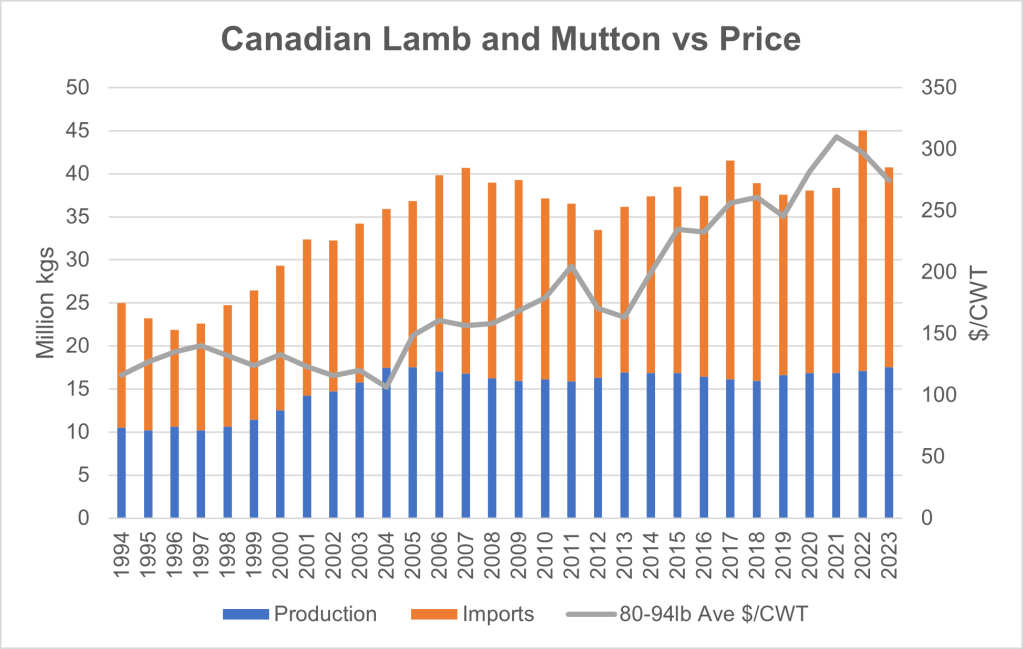

In recent years, lamb production in Canada has shown relative stability with minor fluctuations. The production increased slightly from 17.1 million kg (thousand tonnes) in 2022 to 17.52 million kg in 2023 (Figure 12). Most of the change in overall supply from year to year comes from changes in volume of imported product. Price has been on an upward trend overall and does not always decrease when supply increases or increase when supply decreases indicating that forces outside of our Canadian market affect price.

Imports by Country

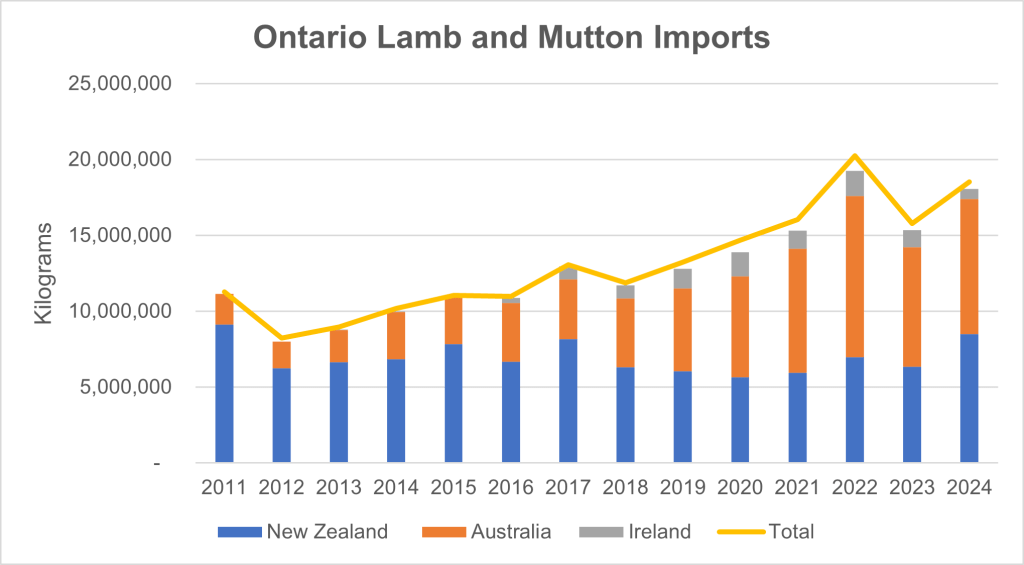

Australia and New Zealand dominate the Ontario lamb and mutton import market, with these countries collectively accounting for most imports (Figure 13). Since 2013, Australia has doubled its market share in Ontario. In 2024, Australia supplied about 48% of Canada’s lamb and mutton imports, while New Zealand provided approximately 45.8% and Ireland supplied about 3.7%. The difference between the line and the top of the bar in Figure 13, is indicative of imports from other countries.

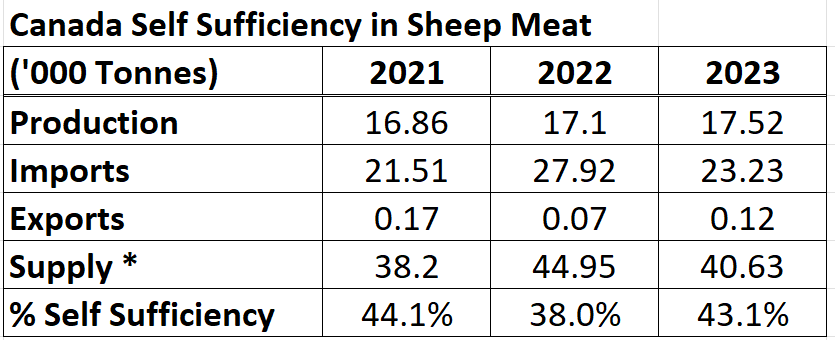

Self Sufficiency

The Canadian sheep industry generally only supplies about 40% of the lamb and mutton consumed in Canada. Statistics Canada estimates supply and disposition of lamb and mutton in Canada. Table 2 shows that in 2023, lamb and mutton production estimates increased to 17.52 thousand tonnes, up from 17.1 thousand tonnes in 2022 and 16.86 thousand tonnes in 2021. Along with this increase in production, imports decreased resulting in an improved self sufficiency due to a smaller overall supply of lamb and mutton.

The net supply of lamb and mutton, which combines production and imports while subtracting exports, was 40.63 thousand tonnes in 2023. This figure represents a decrease from 44.95 thousand tonnes in 2022 but is still higher than the 38.2 thousand tonnes recorded in 2021.

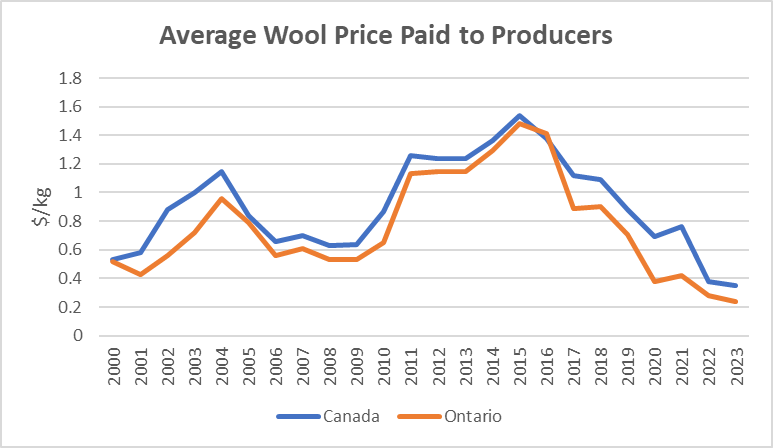

Wool

The average price of raw wool has seen significant volatility over the past two decades, with a marked decline in recent years. Figure 14 shows how, since 2016, wool prices have decreased substantially, reaching their lowest levels since the turn of the millennium. In 2023, the average price of wool in Ontario was $0.24/kg, compared to Canada’s national average of $0.35/kg. This indicates that Ontario’s wool prices were 68.6% of the national average, reflecting a consistent pattern of lower pricing in the province compared to the rest of the country. Wool has become waste to some operations as trucking costs overtake wool value.